After the longest lapse in the history of the National Flood Insurance Program in October and November, the program that provides $1.3 trillion in coverage to more than 4.6 million homeowners is set to expire again on Jan. 30, 2026.

Although the National Association of Realtors and other real estate industry groups expect that Congress will pass a temporary reauthorization of the NFIP before then, they’re practically begging lawmakers to come up with a long-term solution.

“It is time to end the cycle of short-term extensions and program lapses that fuel instability in real estate markets and communities dependent on reliable flood coverage and mitigation support,” a coalition of groups representing mortgage lenders and insurers wrote Congressional leaders on Dec. 2. “Bipartisan Congressional advancement of a long-term reauthorization that includes practical reforms will help stabilize housing and insurance markets while risk management technology and capabilities continue to improve.”

During the most recent government shutdown, the program lapsed for 43 days. While existing NFIP policies remained active and transferable and some lenders suspended the requirement for homebuyers to purchase flood insurance, early reports suggest that the lapse “may have adversely affected the housing market in some states, such as Florida,” the Congressional Research Service said in a Dec. 2 report.

While the program has been criticized for allowing homeowners to rebuild in flood-prone areas at taxpayer expense, the NFIP is also routinely swept up in unrelated partisan disputes over the federal budget.

Since Sept. 30, 2017, Congress has enacted 34 short-term reauthorizations of the NFIP, the Congressional Research Service noted. Uncertainty and lapses are a feature of the program, not a bug.

During the government shutdown of 2018, Congress approved a standalone NFIP extension that kept sales from being derailed. But the program lapsed four times between 2008 and 2012, and the 2010 government shutdown and NFIP lapse derailed an estimated 1,400 home sale closings a day, the Congressional Research Service noted.

Groups representing mortgage lenders and insurers acknowledge that long-term reauthorization of the NFIP will require bipartisan agreement on “practical reforms” to “help stabilize housing and insurance markets while risk management technology and capabilities continue to improve.”

That includes modernizing Federal Emergency Management Agency (FEMA) flood maps to cover the entire country and account for all types of flooding, including rainstorms, groups, including the American Bankers Association, American Land Title Association and Mortgage Bankers Association, maintain.

A 2023 study in Nature Climate Change estimated that unrecognized flood risks driven by climate change mean U.S. homes may be overvalued by $187 billion — a “climate housing bubble.”

The peer-reviewed study laid much of the blame for the tendency to underestimate the risks posed by climate change on outdated flood insurance rate maps and inconsistent state-level flood risk disclosure laws.

Thanks in part to outdated flood maps, 83 percent of the overvalued properties at risk of flooding identified by the study were outside of Special Flood Hazard Areas (SFHAs) — 100-year flood zones mapped by FEMA.

Climate housing bubble hotspots

Median property-level overvaluation as a proportion of properties’ current fair market value | Source: “Unpriced climate risk and the potential consequences of overvaluation in US housing markets,” Nature Climate Change, Feb. 16, 2023.

The private sector has been trying to fill the knowledge gap, with companies like Cotality, Attom and First Street providing climate risk data at the individual property level to lenders, investors and homeowners.

Although Zillow recently opted to stop providing such data with each listing, it continues to link to First Street’s website. Redfin continues to display climate risk data with individual listings, citing its value to homeowners and homebuyers.

“Homeowners should think about natural disasters as an ongoing risk and have an action plan in case catastrophe strikes,” Redfin Chief Economist Daryl Fairweather said in a statement.

Groups representing mortgage lenders and insurers say they would also like to see Congress back “a public-private partnership between the NFIP and private flood insurers to expand coverage options and improve affordability, particularly outside high-risk zones.”

In addition to better insurance, homeowners and communities need funding to implement flood mitigation efforts that would reduce risk to property owners, save lives and lower insurance costs, they maintain.

Every $1 invested in mitigation yields $13 in avoided losses, the groups said, citing research by the National Institute of Building Sciences.

In a bulletin to members, the National Association of Realtors said it’s maintaining regular communication with Congressional leaders and the White House, and expects lawmakers will pass a short-term reauthorization of NFIP before it lapses again on Jan. 30.

If that doesn’t happen, existing NFIP policies will remain in effect, and sellers can assign their NFIP policy to buyers, maintaining coverage on the property without the need to issue a new policy. But the NFIP program won’t be able to issue or renew flood insurance policies after Jan. 30 unless it’s reauthorized.

Private flood insurance that’s not backed by NFIP would not be affected, and NAR recommends visiting state insurance department websites to shop for private insurance in the event of another lapse.

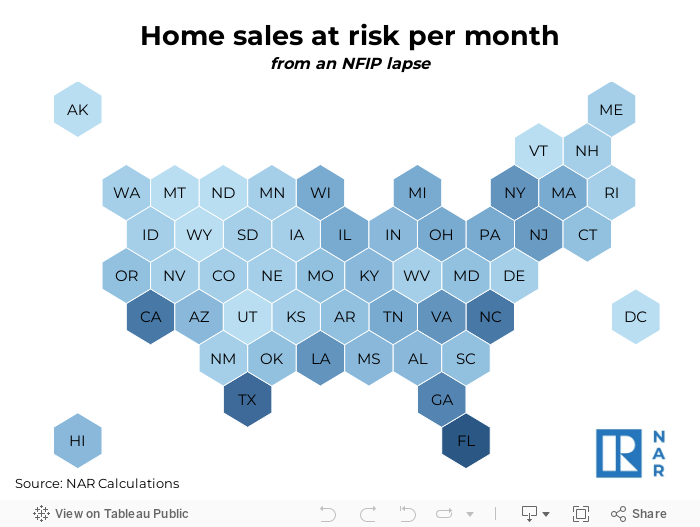

NAR estimates that about 41,300 home sales per month depend on NFIP policies, with Florida (14,870 sales per month), Texas (3,590 sales) and California (1,680) the states that are most dependent on the program.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.